FOCUS In the busy times we live, sometimes we have to stop and assess what we are doing and how we are doing it. To accomplish things as easily as possible, we must learn to focus. The dictionary defines focus as: A center of interest or activity Close or narrow attention with concentration To direct toward a particular point or purpose. Notice how all 3 definitions point to the same thing. Get something in your mind and concentrate on that one thing. With all the distractions of life, it is truly not easy. Some people have dinging sounds go off each time an email comes in or their phone beeps as messages come in. Social media updates can keep you distracted all day. These probably need to be minimized or eliminated, particularly when at work. In the book “Limitless”, Jim Kwik talks of how we are covered up in what he calls digital distraction and digital deluge. No one can take in all the information being shoved at us from all directions. I do not have sounds come in each time a new item comes into my email box or a new message comes in. I receive approximately 300 emails a day, and that is after using spam filters are used to forward from one email service over to Gmail which filters it again. If I stopped to look at every email that came into my inbox, I would not accomplish one thing during the day. Do I miss some important emails? Perhaps a few, but I don’t spend time watching emails. I check them in the morning, at noon, and then again between 3:30 and 4:30 in case of any major issues at work. If it is important and I miss a message or email, the phone will ring. So try to turn off many of the distractions and constant advertisements that bombard us from television, web browsers, and social media. Not all of this is bad, but we can be quickly overloaded with all these attempts to distract us. I read recently that the average person who watches 2 hours of tv and browses the internet and social media 1 hour a day is faced with approximately 3,000 advertisements. This includes those on the radio and the billboards you see as you drive down the highway. To get things done, we need to funnel our attention to the thing at hand. Whatever it is, we need to really put our full power and concentration into the thing we are doing. When working, I try to always remember the admonition in scripture to do things the very best we can. Col 3:23 And whatsoever ye do, do it heartily, as to the Lord, and not unto men; To get our full attention on the task at hand, we must learn to shut off distractions and focus on what is important. Work deserves our full attention, but we can’t be doing 5 things at once. The human mind was never designed to multitask. We are not like computers who can switch back and forth and keep up with where we were. Each time you are interrupted, your productivity goes down. I was the data processing manager for a large hospital for 10 years. A lot of people were employed over those years, and many were very disorganized. I particularly remember this one lady who could not be effective at work. All she could do was discuss her family issues with her husband and 3 kids. When she went home at night, she was ineffective there as all she could do was complain about the work and the people at work. One day we discussed her issue and I explained that when she was at work, she needed to focus on work. And when she went home, focus on family and forget work. After our discussion, her productivity increased and she was a much happier person both at work and at home. All of us are tempted to let distractions defeat us. We need to put everything to the side and be in the moment. When with your kids, don’t be texting or watching television. (unless doing it as a family). So if you are out shopping, don’t be concerned with work or other concerns. If you are having time with your kids or grandkids, be in that exact moment. When at church, put your full attention to worshipping the Lord and keep your mind on God, and don’t think about what activities may be going on after church. And when working, concentrate on the task at hand. List out your to-do list, prioritize, and pick out the specific thing that needs to be accomplished. Always keep in mind that most likely you will only accomplish 2 or 3 things in a day. Be sure you are on the important things. And then only focus on the task at hand. By minimizing the distractions, and putting our focus on the one thing at hand, we can accomplish more and have a more successful day. Try cutting off the digital distractions and see if your productivity is not improved. It will settle your mind and you will not be nervous about all the things pending to be done. Perhaps you can turn off your phone during certain hours of the day. Not everyone can, but if possible, it can help you to focus at a high level. What will be the results of minimizing distractions and focusing on the task at hand?

List of All Investment Articles List of All Minimalism Articles Internet Direct Laptops

0 Comments

Differences in Faith and Fear I try to constantly learn more to increase my Spiritual relationship with the Lord. Anything that really touches my heart makes me study the topic even more. Last week, Stan Clines, my good friend and fellow church member, brought a super devotion on Fear and Faith. He pointed out that they are totally unalike. Faith is from God; Fear is from Satan. Definition of FAITH: Heb 11:1 Now faith is the substance of things hoped for, the evidence of things not seen. Definition of Fear: an unpleasant often strong emotion caused by anticipation or awareness of danger anxious concern reason for alarm caused by listening to liars We all have heard the words Faith and Fear all our lives. However, I had never realized that the two words are polar opposites. They are 180 degrees apart. If Faith is the north pole, then fear is the south pole. How many verses do you think the word “fear” appears in the bible? 385 verses. “Feareth” is in an additional 20 verses, while “faith” is found in 231 verses. God’s desire for his people is to spurn fear and turn in trust by faith to him when we face weak times. God does not want us to be people of fear. In every instance when God or an angel appeared to men in the Old and New Testaments, some of the first words they spoke were “Fear Not.” Here are some verses from the Old Testament Gen_15:1 After these things the word of the LORD came unto Abram in a vision, saying, Fear not, Abram: I am thy shield, and thy exceeding great reward. Gen_26:24 And the LORD appeared unto him the same night, and said, I am the God of Abraham thy father: fear not, for I am with thee, and will bless thee, and multiply thy seed for my servant Abraham's sake. Exo_20:20 And Moses said unto the people, Fear not: for God is come to prove you, and that his fear may be before your faces, that ye sin not. Jos_8:1 And the LORD said unto Joshua, Fear not, neither be thou dismayed: take all the people of war with thee, and arise, go up to Ai: see, I have given into thy hand the king of Ai, and his people, and his city, and his land: Same Words Found in the New Testament Mat_1:20 But while he thought on these things, behold, the angel of the Lord appeared unto him in a dream, saying, Joseph, thou son of David, fear not to take unto thee Mary thy wife: for that which is conceived in her is of the Holy Ghost. Mat_28:5 And the angel answered and said unto the women, Fear not ye: for I know that ye seek Jesus, which was crucified. Luk_1:13 But the angel said unto him, Fear not, Zacharias: for thy prayer is heard; and thy wife Elisabeth shall bear thee a son, and thou shalt call his name John. Luk_1:30 And the angel said unto her, Fear not, Mary: for thou hast found favour with God. Luk_2:10 And the angel said unto them, Fear not: for, behold, I bring you good tidings of great joy, which shall be to all people. When you look at the men and women of faith in the bible, you see people that exhibited little fear. Heb 11:8 By faith Abraham, when he was called to go out into a place which he should after receive for an inheritance, obeyed; and he went out, not knowing whither he went. Heb 11:9 By faith he sojourned in the land of promise, as in a strange country, dwelling in tabernacles with Isaac and Jacob, the heirs with him of the same promise: Heb 11:10 For he looked for a city which hath foundations, whose builder and maker is God. Heb 11:11 Through faith also Sara herself received strength to conceive seed, and was delivered of a child when she was past age, because she judged him faithful who had promised. Heb 11:12 Therefore sprang there even of one, and him as good as dead, so many as the stars of the sky in multitude, and as the sand which is by the sea shore innumerable. Time does not allow us to review the dozens of examples of faith in the bible. Chapter 11 of Hebrews covers many men and women who God commended for their faith. You look at young David facing Goliath on the battlefield with a sling and a rock. You see men like Daniel thrown in a den of lions but by faith coming out unhurt the following morning. What sets these people apart from others? Undying faith in the omnipotent Jehovah God. Let’s all get rid of fear in our lives. Let’s get up each day, look to the Savior of our souls, Jesus Christ, and seek help each day so that we too can live without fear. Fear is from Satan and is not for the child of God. 1Jn 4:17 Herein is our love made perfect, that we may have boldness in the day of judgment: because as he is, so are we in this world. 1Jn 4:18 There is no fear in love; but perfect love casteth out fear: because fear hath torment. He that feareth is not made perfect in love. So, if fear is overtaking us, we need to develop a higher level of faith in God. Read your bible. Be in constant prayer on a daily basis with the Lord. Heb 11:6 But without faith it is impossible to please him: for he that cometh to God must believe that he is, and that he is a rewarder of them that diligently seek him.

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are of my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. WHY I LOVE PASSIVE INCOME Few people realize the importance of Passive Income. In life, we must either work for a paycheck, or we can wisely invest and let those investments pay us. Last year I had virtually no substantial income from dividends. By purchasing a lot of Growth Dividend Stocks, CEFs (Closed-End Funds) at huge discounts to Net Asset Value, and some Preferred Stocks, we have now over $70 per month coming in. We are planning for over $100 per month in the next six months, with a goal to get above $500 within 2 years. Article on DGI Dividend Investing (Click here) Article on Closed End Funds Article on Preferred Stocks Passive income makes you money while you sleep. We were taught in school to work hard, to make good grades, go to college, and then get a good high-paying job. Put your money into the 401-K or IRA and then retire at 65 and be happy. How does working your life away for 45 to 60 years sound like a good plan? If we can leverage some passive income to our advantage in our 20’s and 30’s, there is no reason we should have to work most of our lives. If you are much older, it still works to your advantage, so keep on reading. You are never too old to develop passive income. Passive income is income that you don’t work for on a daily basis. It can come from dozens of sources. Some may have required earlier work, but it is mainly money today for efforts put in the past. Probably the most common passive income is interest from your savings account. Here is a short list of some Passive Income sources. Common Passive Income Streams

We did articles on dividend-paying stocks and how to pick some good ones. One was on the Dividend Aristocrats and the other was on the Dividend Kings. Check those out for good leads on stocks that will not only pay dividends but grow in value also. Dividend Aristocrats Dividend Kings Why Passive Income? - SIMPLE AND REQUIRING NO INVOLVEMENT You wake up and money flows into your bank accounts and all you do is watch it grow. My friend Joshua King started writing content at the age of 36 and now has over 140 Kindle books bringing in a monthly income of over $650. With the compounding effect that this has, he will reach over $1,000 of book-producing revenue each month within five years. So being a writer can clearly be a method of obtaining passive income. Joshua King is the one who got me started on the quest for Passive Income. This next book link is one of the top 5 most important Investment Books I have ever read. Joshua wrote a 319-chapter book on just Passive Income named: The Biggest Book on Passive Income Ever. You can buy it at Amazon using this link: Biggest Book on Passive Income To be able to write on topics such as investing, we must study and read every day. There is no substitute for filling our minds with new information that is pertinent to business and investing today. Much bad information is there too, so learn whom you can listen to and whom you can not. Who should pursue Passive Income? I think we all should. Producing more income, allows us to give and help others in need. And having a steady source of income is very comforting in tough times. List of All Investment Articles List of All Minimalism Articles Internet Direct Laptops

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are of my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. Book Review – Limitless by Jim Kwik This is one of the greatest books I have ever read. It makes you question all the ways you have been trained to think and learn and apply new methods. Get the book on Amazon at Limitless I was hesitant to dive into this book as it seemed a little far-fetched to me initially. This book is not about finances, but it is all about how to think and get rid of ‘Limiting beliefs’ about yourself. Doing this will help you in making financial decisions and learning to live a full complete life. Few books have ever left me with such a strange feeling as this one has. Richard Kiyosaki’s Rich Dad Poor Dad made me question my ‘limiting beliefs’ on investments, but this book opens up many foods for thought. How much of your brain are you using? And could you easily be learning much more and much faster? This book has a lot of answers. Jim Kwik tells his life story of having a fall when he was very young, and it impaired his ability to think and learn. He earlier could not learn like all the other kids, but after his accident things just did not make sense. His teachers were so discouraged with him that one of them nicknamed him “The boy with the damaged brain.” NEVER tell a child something like this, as a child takes what they are told as fact. That is why so many movements today are trying to indoctrinate young children with false teachings since they don’t yet have the maturity to make good decisions and know the truth from a lie. If a wrong thing is taught (a lie) and a person of authority teaches it, it is assumed to be true by a young person. Jim Kwik was hurt by the teacher’s comment, and it set him off on the path that made him have a horrible time in school. Even in college, he simply could not learn things being taught by current teaching techniques. Then he found out he needed to learn “How to Learn.” That changed his life, and now he is a coach to people all around the world and a motivational speaker. What I learned from “Limitless” by Jim Kwik: Our most precious gift is our brain. It allows us to learn, love, think, create, and even experience joy. It is the gateway to our emotions and it allows us to innovate, grow and accomplish great things. Humans (and our brains) are not computers and we can not multi-task and be effective like a computer can. We need to prioritize things and concentrate on the one thing at hand. Focus is crucial. Jim says that part of the reason we can not learn effectively is due to the four digital enemies of our minds. Digital Deluge – we have an almost unending flood of information that we do not have the time to process it all. This results in anxiety, feeling overwhelmed, and sleeplessness. Digital Distraction – We have this fake pleasure from all the digital distractions about us. Our emails ping and our phones ding with messages. We have so many distractions that it is hard to accomplish anything. We must limit this so we can be in the moment and do what we are doing without constant distraction. Digital Dementia – We can let our memory/brain become of no use by thinking every answer can be googled. We don’t process what is happening and come to our conclusions as we should. We are effectively outsourcing our brain to the internet, and not all things are facts on the internet. Digital Deduction – We let our computers make deductions for us. That is for us to assess and do, not some google algorithm program. We have lost the ability to process information and come up with deductions. Don’t let machines make your deductions for you. Mindset is so important. Mindset is the held beliefs, attitudes, and assumptions we create about who we are, how the world works, what we are capable of and deserve, and what is possible. Jim used ‘superheroes’ in his life to protect and project himself. He wanted to be a hero like Spiderman. Most everyone has some kind of ‘limiting beliefs.’ We are taught certain things about our limitations and we take those to be fact. In the book, he tells the story of Roger Bannister. Back in the 50s, it was a known ‘belief’ that no one could ever run a mile in less than 4 minutes. But in 1954, Roger ran it in under 4 minutes. 46 days later another person ran it faster than he, and since then, over 1400 others have run a sub-4 minute mile. See how we need to not limit what we can do. With the right mindset, we can be limitless. If we have these limiting beliefs, it is more than just in our heads. John Hopkins found that people with positive attitudes are 13 percent less likely to have heart attacks. Optimism can increase our life span, lower the rate of depression, and lower levels of distress when they come. We even have greater resistance to the common cold and have better coping skills during hardships. We need to reframe our limited beliefs by first identifying the limiting belief and getting to the facts causing those limiting beliefs. Overcome those with a new belief. Jim identifies the 7 Lies of learning. Lie no 1: Intelligence is fixed. It is not fixed and we can continue to learn. Lie no 2: We only use 10% of our brain. We can not honestly determine how much of the brain is being used, but we can stretch ourselves and start using all of our brain. Lie no 3: Mistakes and failures. They do not doom us. We need to learn from each one. Albert Einstein once said, “People who never made a mistake have never tried anything new.” We make mistakes and we need to learn from them and move on. Lie No 4: Knowledge is Power. While not totally wrong, we must learn and take that knowledge and apply it in some action for it to become power. If you do not apply the knowledge, there is no power in just the knowledge. Lie No 5: Learning New Things if Very Difficult –The truth is learning will not always be easy, but the effort pays dividends. Learning is a set of methods and a process that becomes easier than you know how to learn. Lie no 6: Criticism of Other People Matters. We must learn to let go of the fear of criticism from others. Lie No 7: Genius is born. Genius is learned and there is always a method behind what looks like magic. Genius is not born but made through deep practice. To learn and grow, we need to use The Three M’s: Mindset Methods Motivation What we eat can help fuel the brain. Here is a list of top brain foods: Avocados, Blueberries, Broccoli, Dark Chocolate, Eggs, Green Leafy Vegetables, Salmon, sardines, Caviar, Turmeric, Walnuts, and Water (Brain is about 80 percent water so dehydration can cause brain fog and fatigue. Well-hydrated people score better on brainpower tests. To become limitless, we must learn to FOCUS. We must limit distractions and calm our busy minds. Anxious minds can cause us to overthink. Things like yoga and meditation can help to calm our minds. 3 things to help calm the mind:

Memory – You must train your memory. There is a whole set of chapters on this. But we can teach our minds to remember things. We may need to relate the thing or person’s name to a place or even a smell. You can make the words into a story to help you remember each name in a list. Use the mnemonic device with the letters: MOM M: Motivation O: Observation M: Methods One of the best quotes in the book is from Mark Twain: The man who does not read good books has no advantage over the man who can’t read them. Speedreading. Many ideas are given on how to speed up our reading. One is to remember that probably the last time you took a reading course was the fourth grade. When we first started reading, we had to ‘vocalize’ each word and speak it to the teacher. Without realizing it, our brain may be vocalizing each word causing us to slow down. Also by using your finger on each line as we read, we can drastically pick up speed. Words begin to flow and we don’t have to read each word to understand the sentences. It simply ties together as the commas and periods are there but not processed in our minds. This is important and it has improved my reading speed to almost double. In conclusion, we need to learn to think and use new methods of learning. What you were taught may not be your optimal learning method. Jim Kwik has caused me to question everything and try new methods. Learning is a life-long process. We must continue to grow and learn. The brain is a muscle, and it needs a workout. People who continue to grow and learn are much less susceptible to brain diseases such as Alzheimer's. List of All Investment Articles List of all Minimalism Articles Internet Direct Laptops

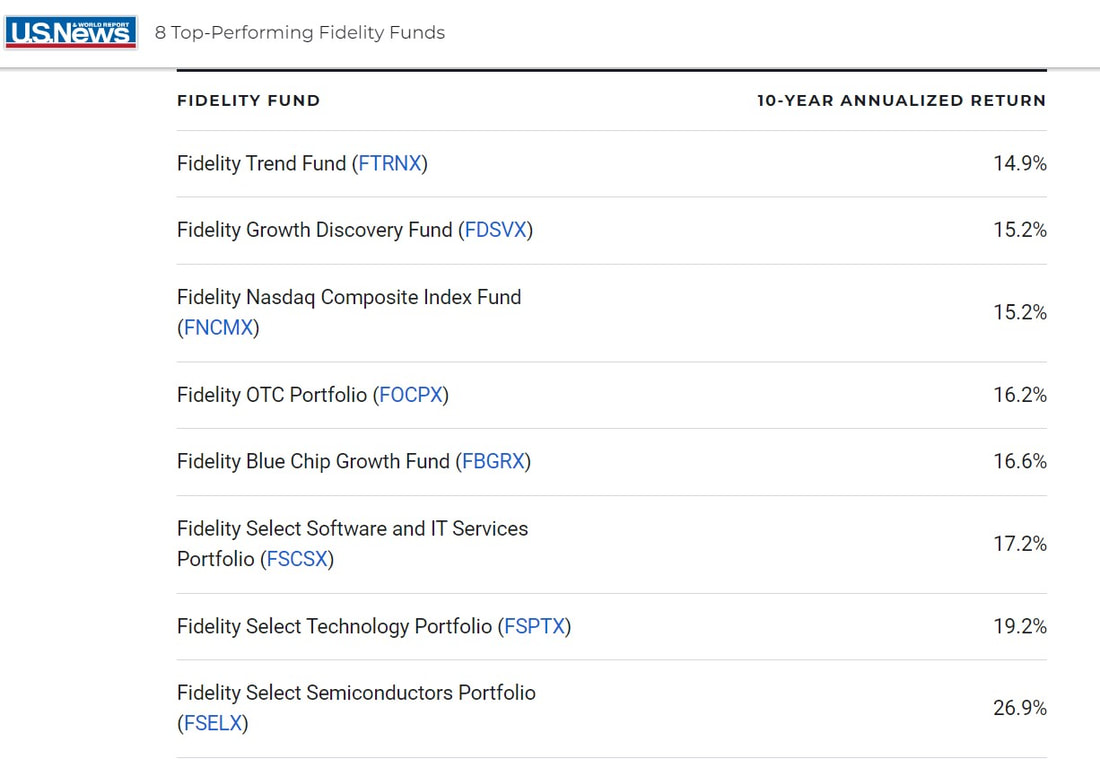

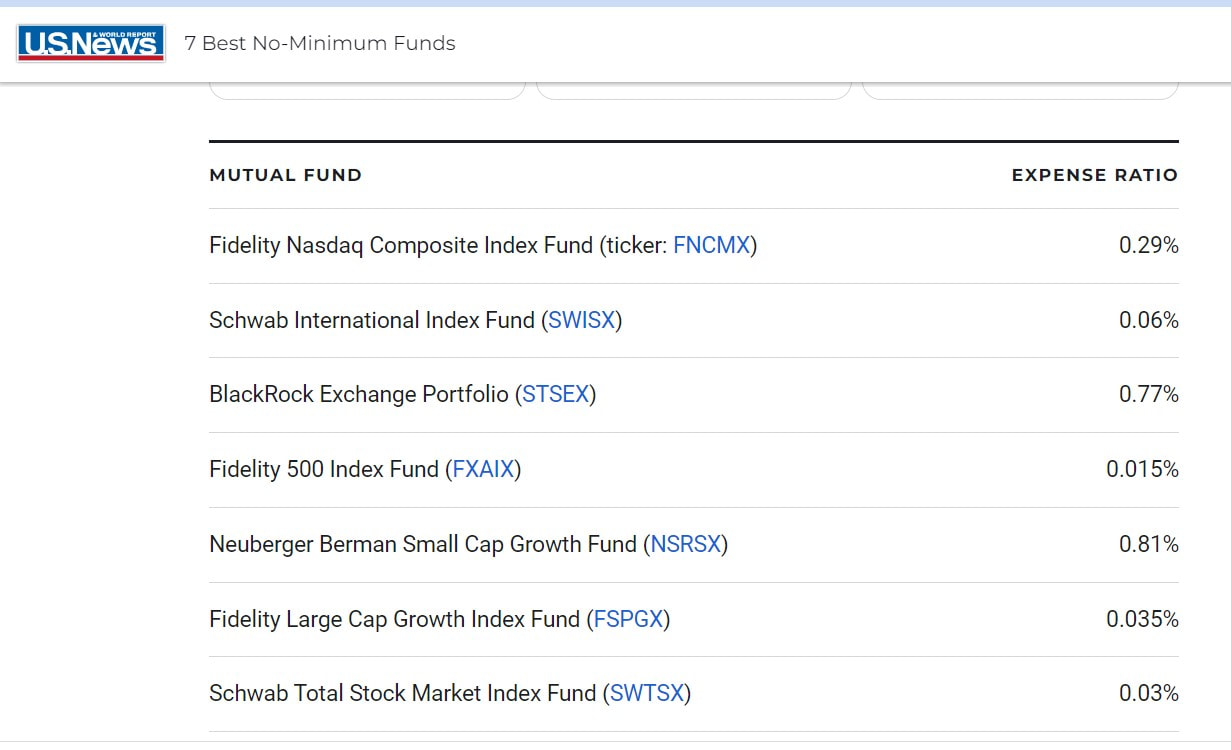

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. The purpose of my blog is to help people find ways to invest successfully. I have tried most methods of investing, and some have been very rewarding. One, in particular, is investing in Dividend ETFs that use covered call options to bump the yield Read about it in the next Link. Investing with High Yield ETFs that use Covered Calls We have articles on using Preferred Stocks (another of my favorites) and Business Development Companies. Another good returning investment type is Real Estate Trusts. (REITS) But it does take time to research all these types of investments. I watch a lot of investment videos on YouTube. But the one podcast that has helped me the most is the Dave Ramsey show. Dave Ramsey shows clearly that to get a good retirement, you have to have a change of mindset about money. You have to quit letting the world push you around and steal all your money by credit card offers. He has a simple 7 baby step program that works. You first set up an Emergency Fund of $1,000 and cut up your credit cards so you never again use debt. Then you attack the debt with gazelle intensity. Read all about it in the review of his book: The Total Money Makeover by Dave Ramsey After you get out of debt, he recommends investing 15% of your money in 4 types of simple Mutual Funds. I recently watched a show where he explained the four types of funds. His meaning of Growth and Income is not like the standard definition but it works. Large Growth Mutual Fund Large Growth and Income Aggressive Growth Fund International Fund In his explanation, he said the Large Growth Fund is the Large Cap stocks in funds such as an S&P index mutual fund. The Large Growth and Income encompass some mid-sized companies and includes Mid-Cap Stocks. The Aggressive Growth Fund is about Small-cap companies and tech stocks that are very volatile, but offer substantial upside in good years. International Mutual Funds are made up of all the non-US companies with varied contents. I have found that the US seems to have many of the stronger companies with high profits, so I lean towards buying Global Funds which include foreign and US companies. Realize that while they may do better than straight International if America has a bad year and Japan and China do well, you could be better off in International. He urges you to look at the charts on these and be sure they are above the line of the average. On the top two, look at the S&P 500. On the small cap you probably want to compare to the Russell 2000 small cap graph. If you are using Fidelity, they do that for you. Your goal is to get managed funds above the ‘average’ for that stock group. Of course, on international funds, you have to look at the average of all the International fund averages. He says to focus on the 10-year returns, not the hottest thing this year. If they haven’t been around 10 years you probably need to look for another. There are many, many well-managed mutual funds. Use the stock/mutual fund screeners to narrow your focus. What is great about this is you are not limited to owning just 4 mutual funds, but Dave Ramsey wants you to be 25% into each category. The larger ones are less volatile and more steady. The bottom two may be rocky some years but may really do well in other years. Each year he recommends selling off and resetting the balances to keep the four categories about equal. So if it is this simple, how do we do it? Well you have to find those kind of stock funds. Then the next thing that came up when I started looking at the funds was the minimum investment. A lot of the great 5-star funds are great, but they have $2500 or $10,000 minimum investment. Having an account at Fidelity, I began my search there. I found that most if not all Fidelity Mutual Funds have no minimum investment restrictions. So I want to give you the list of the ones that I chose for myself and my wife that fall into the Dave Ramsey categories. Some have done better than others, but all this year are doing well. If I accidentally left an ETF in these I apologize.  Do you need this many? Of course not. But we have holdings in all of these, and you can find at least one of the types of funds he recommends on each category. If you want to just start with one, I would recommend going to with the S&P 500 Index fund or the Blue Chip Growth. Last week US News did an article on 8 great Fidelity Funds to own. These are all really good ones. I try to seek those showing a 10 year average growth of 12% or more. ALL of these do. Link to US News Article on 8 Great Fidelity Funds  So can we find 4 or 5 Fidelity Funds to accomplish what Dave Ramsey recommends? I think the answer is clear that we can. I will give you a pick of two for each of his categories if I could only buy 4 funds. Large Growth: FBGRX – Fidelity Blue Chip Growth Fund FSKAX – Fidelity Total Market Index Growth and Income: FSELX – Fidelity Select Semiconductors Portfolio FSVMS – Fidelity Mid Cap Growth Aggressive Growth: FOCPX – Fidelity OTC Portfolio FCPVX – Fidelity Small Cap Foreign Fund: FZILX – Fidelity Zero International Fund FIVFX – Fidelity International Cap Appreciation Another good option might be to buy all 8 of these which will give you even more diversification. You could if you desire buy 3 or 4 of each category as I have done. If I have learned anything from Dave Ramsey, it is that knowledge is only 20% of success. DOING IT is 80%. So don’t sit on the sidelines but get in and consistently invest month after month. Time is on your side. Remember that you can divide the return into 72, and it will tell you how long it will take for your money to double. So if you get an 8% return, it just takes 9 years to double your money. But if you can average 12%, it is every 6 years. Article on the Rule of 72 Another article came out last week that relates to my plan. It was also by US News Investing and it was about the 7 best mutual funds to own that have no minimum investment. So you could consider using some of these rather than the Fidelity Funds if you prefer these companies.  No matter if you are trying to use the Dave Ramsey plan or your own, mutual funds are good investments and require minimal maintenance on your part. Each year you should look at the graphs on the growth of your fund and if it is lagging the industry average, then sell it and move into another fund that is above the average line. I hope this helps and gives you the incentive to get started in mutual fund investing. Investment Articles Minimalism Articles Internet Direct Laptops

Investment Categories DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. In one of our earliest articles post on investing, we covered how that one of the best methods to invest is by using an IRA account. There are many advantages of this over just opening a brokerage account. One of the biggest is the tax ramifications of buying and selling stocks, mutual funds, or ETFs. (Exchange Traded Funds). We discussed bonds in a separate article. Definition of a Bond These 3 are very similar and are all invested in the stock market. (Some mutual funds and ETFs do invest in bonds.) If you buy and sell in a short window of time (under one year), you have a short-term gain or loss that is taxed at a higher rate than a long-term gain or loss. By investing in a retirement account, this issue is resolved as you simply pay for the gains when you withdraw the money on a traditional IRA, and on a Roth IRA, you never pay any taxes. Roth IRAs are my choice of platform for investing. Today let’s do a short article on the three main investment types sold by brokerages. Stocks, Mutual Funds, and ETFs. STOCKS Stocks are the most highly traded items at brokerages. At the end of 2021, there were 2,529 companies listed on the New York Stock Exchange. On the Nasdaq (smaller companies), there were 3,767. It there are over 6,000 actively traded stocks, most likely no one can tell you for sure what the best buy is on a stock on any day. Some people make their living reading charts and guessing what will happen in the stock market. The volatility of the markets has shown to be high in the first quarter of 2022. An article at Fidelity shows that only 2 sectors made money in the first quarter, those being Energy Stocks and Utilities. The rest lost from 1% to 11.9%. So is now a good time to buy stocks? I would be cautious. Here at the start of 2024, we are at an all-time high on the S&P 500. I have not stopped investing but I am watching the market and using stop-loss orders in case of a downturn. How to Prevent Huge Market Losses in Stocks The advantage of buying when the market is down is that you are buying at a lower price which may recover to its earlier price. However, what if we have 3 to 6 more months and the market loses 20 to 50% more? It could happen. So right now I would be cautious about buying separate stocks. There are so many types of stocks that we will have to get into those in separate articles over the next few months. Some of the most promising stocks are what are called Growth Dividend Stocks. What is DGI Investing These are those that appear to be growing at a good percentage, and at the same time, paying quarterly dividends of up to 13% or more. Most pay 1 to 4%, but some REITs and gas companies are paying very high dividends. Again don’t chase high numbers, but get in the market for the long term. Part of the issue with buying one company’s stock is that if that company begins to lose money or cut its dividend, the price may drop drastically in a short period. So putting all your money in a few stocks is very risky. However, the wider and larger number you have gives you diversification. That brings us to the last two types of investments for this article. MUTUAL FUNDS There are many advantages to owning mutual funds. The first is that they are normally very diversified (many with over 50 to 100 stocks in the fund), and perhaps best of all, they are actively managed by professional fund managers. Many of these are highly trained and seasoned individuals. If you find several different good mutual funds, you can be pretty diversified with just a small amount of investment. Dave Ramsey, the great radio host, believes that a few growth mutual funds purchased yearly will give you an excellent retirement. How can you find those? All of the brokerages have research pages, and they break down the categories of the mutual funds. When buying mutual funds, don’t worry as much about current-year returns as the 5, 10, and 20-year returns. Anyone in today’s market may show a loss, but if the same manager of the fund has had 10 to 15% returns or higher for over 10 years, we can be sure they probably know what they are doing. All we can do is hit the highlights of these 3 investment categories. I will come back and break down each of these and cover bonds in future articles. Another great way to find good mutual funds is to read some financial magazines like Kiplingers. They list some of the best. Kiplingers Magazine ETFs The last category I am going to discuss today is ETFs. (Exchange Traded Funds). These have been around for quite a while and are now the most popular investment type. What is so great about ETFs is that there is a flavor for every kind of investment out there. They base themselves on a segment of the market (or the whole stock market or whole world market) which means they can be VERY diversified. I think a person could easily build a winning portfolio with 5 or 6 ETFs covering the broad markets and some bond ETFs. Over my years of investing, my most consistent return on investment year in and year out has been the total stock market indexes. Review of the book ‘The Little Book of Common Sense Investing by John Bogle. John Bogle is the founder of Vanguard Group and a very intelligent investor who died in 2019. He pushed indexes before we had ETFs and proved that they are a very successful method to invest. His total stock market ETF is VTI and iShares has one called ITOT. Schwab also has a full stock market index which is SCHB. I have a large percentage of my investments in all 3 of these ETFs. These are some of the simpler methods to get into the stock market and buy a fully diversified investment. I found a large number of great articles about John Bogle. Google him and read a few of his thoughts. We will get more details about each of these investment categories and bonds in future posts. List of All Investment Articles List of all Minimalism Articles Internet Direct Laptops

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are of my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. All of us have to start somewhere with investing. I have found that you can be successful in investing by using bonds. Some people feel bonds are the only safe way to invest, but they only offer low rates compared with good years on the stock market. Let's look today at the financial instrument called Bonds. WHAT IS A BOND What are bonds and how do they differ from other financial instruments/categories such as Stocks, Mutual Funds, and ETFs? (Exchange Traded Funds.) Recently, we went over briefly those 3 categories. Today, let’s discuss what bonds are and how they should be used in your portfolio. A bond in simple terms is a debt security. The entity issuing you the bond owes you money. Companies that issue bonds do it to raise money from investors with a promise to pay in a set time period at a fixed rate. (normally a fixed rate.). The time period can be 1, 5, 10, 20, or 30 years. The issuer promises to pay you back the original value of your purchase plus the accrued interest based on the interest rate specified. If you purchased a $100 bond with a 10% rate for the period of one year, at the end of that year you should receive $110 which is the principal of $100 plus the interest of $10. Bonds typically make payments of interest twice per year, but not all do. ADVANTAGES OF BONDS They are obligations of the company, so obligations must normally be paid first in case of bankruptcy. If you buy high-rated bonds (AAA or AA), the chances of default are very slim. But not all Bonds are AAA. Many are B or B- and some are considered junk bonds. Normally a bond yields a predictable income stream and they work well in a portfolio with stocks, mutual funds, and ETFs. As the market dips and you lose 3% of your stock value in the stock market, many times the bonds will go up in value by 1 to 2% offsetting your losses on the stock. Until the year, 2022, that had always been the case in my portfolio. However in 2022, for whatever reason, the bonds have slipped some when the stock market went down. I have not dug into this anomaly, but I think it is related to the Fed upping interest rates during this time of high inflation. In prior years, my results have been that bonds move in opposite direction to the stock market, making them ideal instruments to hold. A mix of 50% bonds and 50% stocks is considered a conservative mix, and if you are very young, you probably would want to stay more like 70% stocks and 30% bonds. Reasoning behind that is the stock market typically recovers from losses, and a young person can weather the long term effects. A person nearing retirement may want to hold 60% bonds and only 40% stock. Only you can assess your risk factor. This has to be assessed before making any investment in any kind of category. KINDS OF BONDS Corporate Bonds – those issued by private and public corporations. High Yield Bonds – Those with lower credit rating making them have to pay a higher rate percentage. Investment Grade Bonds – Less Credit risk associated with bonds in the upper high ratings. Typically AAA, AA, or A rating. Municipal Bonds – These are issued by cities, counties, and states to finance the building of stadiums or other structures such as hospitals. Building of highways is often done with Revenue bonds and these are backed by the revenue from the specific project. Some bonds are NOT SECURED BY ASSETS. These are called General Obligation Bonds, which are a bit riskier. US Treasuries – probably one of the safer long term investments are issued by the Department of Treasury and backed by the government. These have to date been consistent with no defaults. But the day may come where the government may not can pay its obligations as our national debt is escalating at a very high rate. But Treasury bills, Notes, and Treasury Bonds are considered safe investments. Currently, you can open an account at TreasuryDirect.gov and purchase Inflation protected bonds (I-Bonds) that in March of 2024, are now paying a rate of 4.86%. (Check the current rate at TreasuryDirect.gov) This rate is guaranteed for six months and then resets to the new inflationary rate. This past year the rate had been 7.12% and I began purchasing a bond each week and have set a schedule to buy one each week for the next year. You can buy amounts as low as $25 and buy up to $10,000 per household member per year (more if you buy paper I-Bonds with income tax refunds). Verify these facts at TreasuryDirect.gov. In a time of turbulent stock market fluctuations, this is a rock solid investment in my estimation. Consult a Financial Planner or your accountant before making any investment decisions. IN CONCLUSION So to summarize, bonds are considered safer investments than most. You can buy Mutual Funds that are all bonds or you can get a mix of bonds and stocks in various funds. Also there are ETFs for just the bond market. Be sure you understand that these funds and ETFs can lose value or gain value as interest rates go up and down. It is not a lock, whereas if you purchase the bond yourself, it has a guaranteed principal and fixed rate of interest. (most of the time.) We will expand on this topic again in a future article and go into deeper detail. Should you include bonds in your portfolio? I believe the answer is always yes, even if just a small percentage. Investment Articles Minimalism Articles Internet Direct Laptops

Overcoming Obstacles in Life Life is challenging in so many ways. There is always some obstacle in front of us. You may be facing the loss of a job or received a bad report at the doctor. Perhaps your finances are in shambles. Perhaps like most Americans, you have too much month left at the end of the money. No matter the obstacle, we must determine to have fortitude and determination. In life few things are more important than perseverance and determination. As a child, I grew up on a farm and the work seemed to never end. But my dad showed us by example that if you work hard and don’t quit, you can overcome almost any problem in life. I read in a recent book about the sledgehammer approach to dealing with obstacles. The author said whatever is in front of you, use your mental sledgehammer to knock it into manageable pieces. That brings an image to my mind of a rock busted into six or seven pieces. You can only eat an elephant one bite at a time. So, make your elephant bites small. If you have a mountain in front of you, take time to think how to deal with it. Look for ways around it. Maybe you can go right over it. But if not, use the sledgehammer approach and slowly bust it into pieces that you can deal with. I watch Dave Ramsey on You Tube almost every night. He helps people with financial issues that seem overwhelming. If your issue Is financial, look into his 7 baby steps to financial freedom. Check out the article below about his book. It changed my life. The Total Money Makeover by Dave Ramsey. If you are facing a spiritual battle, I urge you find a good church and turn your problems over to Jesus Christ. When you accept Christ as your Savior, you never again face your battles alone. I accepted Christ as my Savior over 50 years ago, and while I have failed God many times, he has never failed me once. My grandson Paul Culver and I have created a website with Bible Studies covering most of the bible. You can signup to have a weekly email on any book of the bible. If you are struggling, sign up for the book of John. It really tells the story of the love of God. KjvBibleStudies.net To signup for the weekly studies, click below and specify the book you want to receive with your name and email. Each Sunday afternoon we send out the next chapter of that book. Signup for Weekly Bible Studies Never give up. Ask God to help you overcome whatever issue you are facing. Learn from your mistakes and don’t repeat the same thing over and over. Dave Ramsey says that the definition of Insanity is doing the same thing over and over and expecting a different result. If what you are doing is not working, it is time to change course. I try to plant a garden each year. I did an article on Why I Plant a Garden last spring. I truly enjoy the fresh vegetables and getting out in the sunshine to do the work. It does take a lot of hard work to raise a garden, but the physical labor is good for me. However, even in gardening, to accomplish your goal, you must overcome obstacles. Last week my Grandson Paul Culver was going to help me rototill the garden to get rid of all the weeds and prepare the soil for planting. However, we found the ground was so hard that the tiller could not break through. So we watered the garden for about 3 hours and that really helped. However, the large Honda tiller we rented at Home Depot ran for 3 minutes and then would never restart. We didn’t give up, although we did have to just take the tiller back last Wednesday since Paul had to work that afternoon. Today my Granddaughter Rachel Culver helped me and we rented another one after making sure it would run. We stayed after it and after a couple of hours we finally had it ready to plant. We worked in a circle breaking the ground, then plowed it north and south to make the rows. It looks great now.  This is another example when things don’t go right for you, you just have to keep on trying. It may have took an extra week, but we still overcame every obstacle in our path. One of my good friends Joshua Becker has been a real inspiration to me over the years. He has the website Becoming Minimalist Check out Joshua Becker’s Article on the 7 Laws of Success. I loved his line about how we can be successful even if we don’t reach our desired results: Success, in my opinion, is controlling what I can (my actions) and dedicating my life to the right things. If I can do that, I'll be pleased with how I chose to live. And I will consider my life a success—regardless of the results. Stay strong and overcome the problems of life with God’s help. Investment Articles Minimalism Articles Internet Direct Laptops

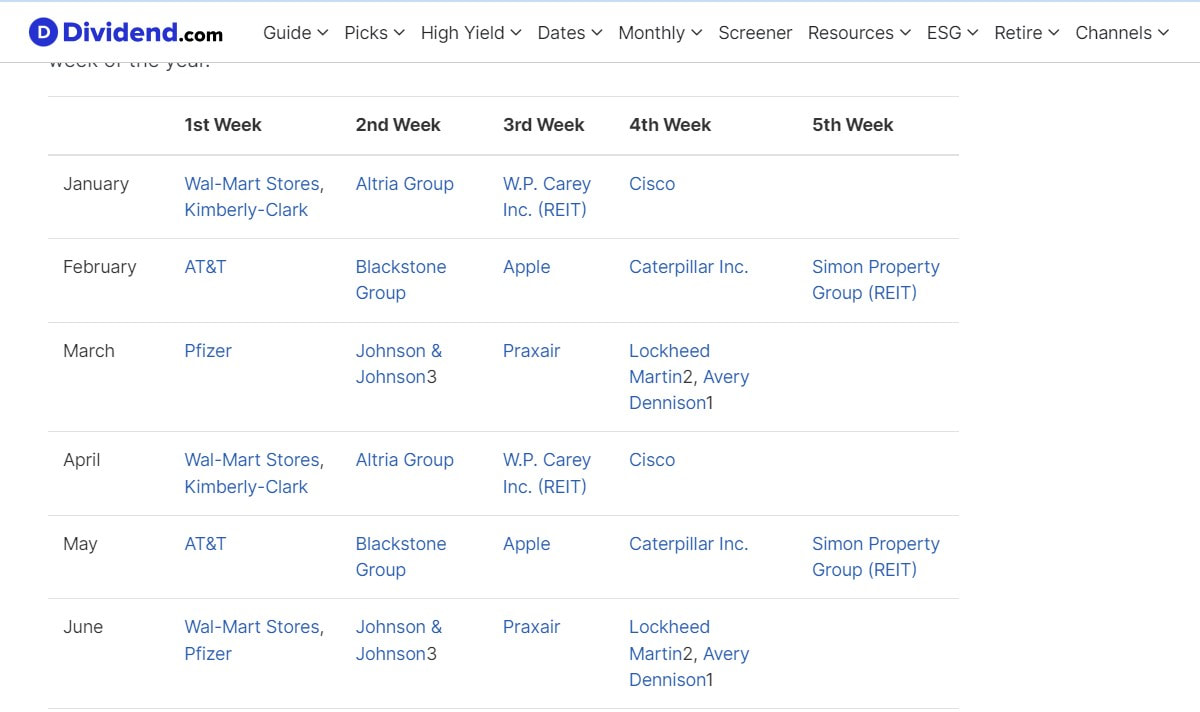

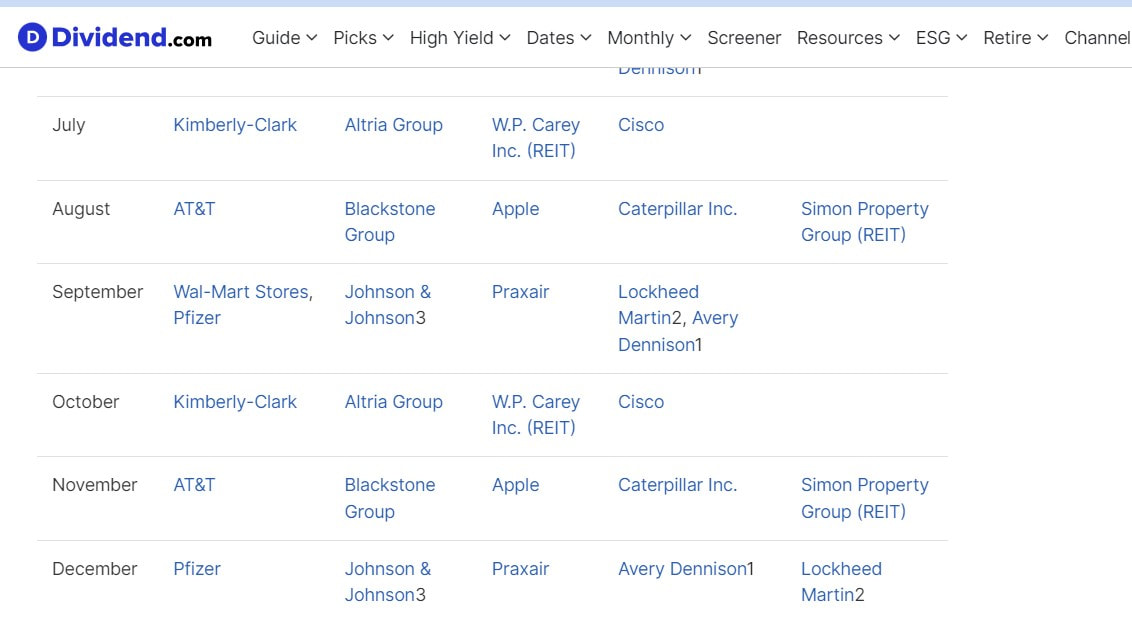

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are of my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. Dividends Every Week of the Year The stock market is full of varying types of investments. One of the most enjoyable investments I have are those that pay dividends. Many of my investments are in ETFs that pay dividends and also individual stocks paying dividends. Article on High-Yielding Dividend ETFs One of the issues that we all have is getting consistent returns. Many stocks pay quarterly dividends, but that does not mean they are at the end of the standard quarters of March, June, September, and December. With a little study, you can get some dividends every month, and now I have found a way to guarantee a dividend every week. A great article was put out by Dividends.com this week on getting paid a dividend every week. Dividend.com Article on Dividends Every Week What is amazing is they figured out how to make it pay every week with just 12 stocks. While some of these are high payers, others are in the lower dividend category. But those that pay the lower dividends many times return growth. Here are the two charts to see the 12 stocks and which pay on which week for the entire year. First pic is first six months. Second is the last half of the year.   If you have a lot of dividend paying stocks, you probably own most of these. I do not own Blackstone Group, Praxair, Avery Dennison, Lockheed Martin, Simon Property Group, or Altria Group. I have no issue with any of these on the list except Altria Group as they sell tobacco products. I try to stay away from anything selling tobacco, alcohol, or is involved in gambling. Let your conscience be your guide. I intend to seek out when Altria Group pays their dividend and find another stock that pays on that same time-period. I don’t think that will be too hard. So consider these in your investment portfolio so you can get some consistent dividends every month. I will incorporate this into my Schwab dividend portfolio where I buy what is called Stock Slices. You can spread as little as $5 into a stock if it is listed as being in their group of Stock Slices. Most S&P 500 stocks are there. If not just buy one share of that stock and add to it by the share. Another option is to buy these at Fidelity.com where there is no limitation on what you can buy by the dollar that I am aware of. Keep on studying and finding good ways to increase your monthly dividends. Dividends are my favorite type of Passive Income. Investment Articles Minimalism Articles Internet Direct Laptops

DISCLAIMER - I am not a Financial Advisor and do not work for any Brokerage Firm. The opinions given are of my own and are not to be used as professional advice. These are my findings and can hopefully help you to make informed decisions on investing. Consult a Broker or Lawyer before making any investment. The Total Money Makeover This is definitely the top most important investment book I have ever read. The Total Money Makeover by Dave Ramsey probably is not your normal investment book in relation to how to invest your money. But if I had not read it or adopted his methods of running my personal life, I would never have had the funds to invest the way I do today. In my previous posts, I have explained how I spent years trying to overcome my huge backlog of debt and failed. Finally, I found this book. It is available in most libraries, but if you want a copy, you can buy it on Amazon: The Total Money Makeover Dave Ramsey has coached millions of people on how to live and manage their finances. His way works. Many do not like his method as it is in your face and he sees no reason to ever use a credit card. (Debit cards are fine.) If his approach is too radical for you, you can try your plan by mixing his method and yours. I did it that way for over 10 years, and if I had not finally said “ENOUGH”, I think we would still be battling a huge unwinnable battle. Each day, Dave Ramsey has a talk show and discusses situations people are in. My wife and I try to watch his show at least 5 times a week. His steady consistent Christian world view really makes sense. If you listen, you will realize your situation is probably not as bad as many who call in. But he gives good sound financial advice. Most spoiled people who think they have to have expensive ‘cars and toys’ find out quickly that he will make you discard those. But hanging on to something you probably should never have bought is not part of his no-nonsense plan. Many like myself got into an over-my-head debt situation by digging a hole with credit cards. Dave Ramsey’s advice is that if you are in hole, stop digging. In simple words, STOP using credit cards. A study of credit card use at McDonald’s found that people spent 47% more when using credit instead of cash. Credit cards give you a false sense of having more money than you truly have. The Total Money Makeover is not just a book of theories. It is a proven reliable method to take on your debt head-on and come out debt-free in as little as 18 to 24 months. Mine was so great it would probably have taken 5 years to use his method. By using part of his methods, we did it in 10 years. However, when we fully adopted the Dave Ramsey method, we were debt-free in 11 months. Dave Ramsey probably has been where you are traveling today. He details how he became a millionaire quickly, and they blew it all and became broke. He got on his path to recovery and got back to being a millionaire several times over. Listen to some of the takeaway highlights I have gleaned from his book. Takeaway # 1 - The problem you are facing is probably not a lack of knowledge. Knowing what to do is 20% of it, DOING IT is 80%. The problem is looking you back in the mirror each day. The issue is YOU. You must get control of things and handle the issue. The cavalry is not coming. If you don’t do a total money makeover, you may wind up with an “Alpo” dinner in your old age. Sounds gross, but if you can’t afford food, you might reach such desperate straits. Takeaway # 2 - You must have a sound financial system. Anyone can blow more money than they make. But a solid plan will work day in and day out. He quotes great investor Warren Buffett who says “When the tide goes out, you can tell who was skinny dipping.” In other words, if you don’t have your finances in control, the ups and downs of life may destroy you. And this goes for investments down the road too. Get on a fully diversified SOLID plan once you are at the point to invest. Takeaway # 3 - Dave Ramsey said in his book that he has never met a millionaire who said they got to their lofty status by using Discover points. I was the world’s worst about thinking the ‘right’ credit card would save me money. Paying 18 to 23% interest is not something this is a help to you. Credit cards are NOT YOUR FRIEND. He points out that you and I probably don’t own any of those 20-story shiny buildings, do we? But Discover bondage and Visa and Mastercard and American Express own hundreds of them. Credit cards are NOT YOUR FRIEND. In his book, Dave points out that CHANGE IS PAINFUL. We won’t change until the pain of where we are exceeds the pain of change. When it comes to money, we can be like the toddler in a soiled diaper. “I know it smells bad, but it’s warm and it’s mine.” But the rash comes eventually and we cry out. Until you have had it trying to do it on your own, you will not win. The Credit card companies have you where they want you. Culture and commercials point to a very different picture than reality. Takeaway # 4 - The Baby Steps 1 and 2 of the 7 Baby Steps to Freedom. This is all about HOW to get things under control. You quit living above your means and you stick to a budget. All expensive toys are liquidated and you drive an old Buick or Honda. (I drove both). Baby Step 1 – Save $1,000 for your starter Emergency Fund. Little expenses come up all the time. If you rely on credit cards, you revert to your old ways and soon you have a bill you can not pay. First, you stop paying anything but your basic bills and minimum credit card payments, and you save up $1,000 to use for emergencies. As Dave says in his book, Murphy (Murphy’s law) does not visit people as often when they are prepared for emergencies. If you have to replace your water heater and spend $400 of your emergency funds, you stop your snowballing (Step #2) and refill your emergency fund. Baby Step 2 - This is the second most important thing in getting out of debt. You list all your debts that you owe, the smallest payoff to the highest. He tells you to not be concerned with interest rates, but to worry about wiping out that first lowest debt. You pay the minimum payments on all the rest and pay all you can on the top debt Once it pays off, roll that money into #2 and it becomes the snowball until all 8 or 10 on the list are eliminated. This really really works from my own experience. You see immediate results and it is encouraging. Dave Ramsey encourages you at this point to revaluate everything, and if you have expensive cars that won’t pay off in 2 years or sooner, then sell those vehicles and drive a cheaper car until you get on your feet. Have a garage sale or get an extra job to help with your snowball. This works great! Takeaway #5 – Baby Steps 3 through 5. Now that your credit card debt is finalized, you come back and get organized with your finances. Baby Step 3 – Save 3 to 6 months of expenses in a fully-funded emergency fund. This is not in an investment account, but rather a readily accessible savings account. Baby Step 4 – Invest 15% of your household income into a retirement account. If you have an employer match on your 401K retirement account at work, you put the full matching amount of money there. If you have additional money left to invest, open a ROTH Ira. That way future earnings will never be taxed. Dave Ramsey recommends buying several mutual funds spread over several growth sections. Find those with 5 and 10-year averages of 12 to 15% on returns. Magazines such as Kiplinger’s and Money Magazine list these, as well as all the big brokerage houses like Fidelity, Schwab, and Vanguard. Baby Step 5 – Save for our children’s college fund. Takeaway # 6 - The Baby Steps 6 and 7. Baby Step 6 – Pay off your home mortgage. This gets you 100% debt free from all creditors. Throughout the book, Dave talks about being Gazelle intense about debt. Read that article when you get the book and realize that the gazelle is not too fast, but he is running for his life. You are too when in these baby steps. He found that families who stayed Gazelle intense about debt were out of mortgage debt in approximately 7 years after they declared war on culture and debt. Baby Step 7 – Build wealth and give. When you reach Baby step 7, you can now live like no one else. You are free to truly live a debt-free relaxing life. Takeaway # 7 - The results: You may read this and say, this plan is too simple. I have been there and done that. I tried multiple variations of Dave Ramsey’s plan including funding my Roth IRAs while in baby step 2. It just does not work. What should have taken me 5 years took me more like 10 because I would not conform to his plan. There is something about being TOTALLY FOCUSED on that one baby step until it is done that makes you more determined. As Dave says over and over “Don’t give up.” There will be down moments when it seems like you are not getting anywhere. But make a graph or a pie chart and shout out when you finish even a percentage of one of the steps. Baby Step 2 on the snowball may take you 2 years, or if you are in horrible shape, it might take 6 years. But it is worth the trouble You will be glad you found this book. If like me, you may just need a little simple guidance to get debt-free. It has been the most liberating thing I have ever experienced regarding finances. Look at the millions of people who have stuck with it and can testify that this plan works. Watch his show on You Tube and after a few weeks, you will see that this plan works. In conclusion, let me say that I am so proud to have met Dave Ramsey. He has been a blessing to millions of people (like myself) who have struggled with debt. This is a great book and while not some super important get-rich-quick investment book, it gives you a foundation to get in a position where you can invest and put your money in long-term safe investments.

|

David ParhamChristian Minimalist and Investor. God guides and helps me everyday. Archives

April 2024

Categories |

||||||||||||||||||||

RSS Feed

RSS Feed